Starting a business involves numerous steps, and obtaining a business license is often a key requirement. However, some entrepreneurs may wonder if it’s possible to secure business insurance without having a business license. Business insurance is essential for protecting your venture from potential risks, such as liability claims, property damage, or unexpected interruptions. While a business license is typically a prerequisite for operating legally, the relationship between licensing and insurance can vary depending on your location, industry, and insurer. This article explores whether you can obtain business insurance without a license, the potential challenges, and what alternatives may be available for emerging businesses.

- Can You Get Business Insurance Without a Business License?

- What Types of Business Insurance Can You Get Without a License?

- Why Do Some Insurers Require a Business License?

- How Does Not Having a Business License Affect Your Insurance Application?

- Can You Operate a Business Without a License and Still Get Insurance?

- What Are the Risks of Not Having a Business License When Seeking Insurance?

- Can you get insurance without a business license?

- Can You Get Insurance Without a Business License?

- What Types of Insurance Are Available Without a Business License?

- Why Do Some Insurers Require a Business License?

- What Are the Alternatives If You Don’t Have a Business License?

- What Should You Consider Before Getting Insurance Without a Business License?

- Can you get insurance for a business without an LLC?

- Do you need business insurance for a small business?

- Can you get in trouble for not having business insurance?

- What Are the Legal Consequences of Not Having Business Insurance?

- How Does Lack of Business Insurance Affect Financial Stability?

- Can You Lose Contracts or Clients Without Business Insurance?

- What Happens If an Employee Gets Injured Without Workers' Compensation Insurance?

- Are There Industry-Specific Risks for Not Having Business Insurance?

- Frequently Asked Questions

Can You Get Business Insurance Without a Business License?

Yes, it is possible to obtain business insurance without having a business license, but the process and requirements can vary depending on the insurance provider and the type of business you operate. While a business license is often seen as proof that your business is legitimate and complies with local regulations, some insurers may still offer coverage to unlicensed businesses, especially if you are in the early stages of setting up your business. However, not having a license could limit your options and may result in higher premiums or stricter terms.

What Types of Business Insurance Can You Get Without a License?

Certain types of business insurance may be available even if you don’t have a business license. For example:

- General Liability Insurance: Protects against third-party claims for bodily injury or property damage.

- Professional Liability Insurance: Covers claims related to professional errors or negligence.

- Commercial Property Insurance: Protects your business assets, such as equipment or inventory.

- Workers’ Compensation Insurance: Required in most states if you have employees, regardless of licensing status.

As a New Business What Are the Odds of Getting Venture Capital Funding

As a New Business What Are the Odds of Getting Venture Capital FundingHowever, insurers may require additional documentation or proof of your business activities to provide coverage.

Why Do Some Insurers Require a Business License?

Insurers often require a business license because it serves as proof that your business is legally registered and complies with local regulations. This reduces the insurer’s risk of providing coverage to an unregulated or potentially fraudulent operation. Without a license, insurers may view your business as higher risk, which could lead to:

- Higher premiums

- Limited coverage options

- Stricter underwriting requirements

How Does Not Having a Business License Affect Your Insurance Application?

Not having a business license can complicate your insurance application process. Insurers may:

- Request additional documentation, such as a fictitious business name (DBA) or proof of business activities.

- Limit the types of policies available to you.

- Charge higher premiums due to perceived risks.

- Require you to obtain a license before finalizing coverage.

Where Can I Find a Searchable Database of Venture Capital Investments by Industry

Where Can I Find a Searchable Database of Venture Capital Investments by IndustryCan You Operate a Business Without a License and Still Get Insurance?

In some cases, you can operate a business without a business license and still obtain insurance, but this depends on the nature of your business and the insurer’s policies. For example:

- Freelancers or sole proprietors may be able to secure coverage without a license.

- Businesses in industries with minimal regulatory requirements might also qualify.

However, operating without a license could expose you to legal and financial risks, so it’s advisable to obtain one as soon as possible.

What Are the Risks of Not Having a Business License When Seeking Insurance?

Not having a business license when seeking insurance can lead to several risks, including:

- Denial of Claims: Insurers may deny claims if they discover your business is unlicensed.

- Legal Penalties: Operating without a license could result in fines or legal action.

- Limited Coverage: Some policies may exclude certain risks if your business is unlicensed.

- Reputation Damage: Clients or partners may hesitate to work with an unlicensed business.

| Factor | Impact on Insurance |

|---|---|

| No Business License | Higher premiums, limited coverage options |

| Proof of Business Activities | May be required for unlicensed businesses |

| Industry Regulations | Some industries may require a license for coverage |

| Legal Risks | Operating without a license can lead to penalties |

Can you get insurance without a business license?

How to Get Sponsors for a Team

How to Get Sponsors for a TeamCan You Get Insurance Without a Business License?

Yes, it is possible to obtain insurance without a business license in certain situations. However, this depends on the type of insurance, the insurer's policies, and the nature of your business. Some insurers may require proof of a business license to ensure the legitimacy of your operations, while others may offer coverage based on other factors, such as your business activities or personal liability needs.

- General Liability Insurance: Some insurers may provide general liability insurance without requiring a business license, especially for freelancers or small-scale operations.

- Professional Liability Insurance: Independent contractors or consultants might secure this type of insurance without a formal business license.

- Home-Based Businesses: If you operate a small business from home, some insurers may offer coverage without a business license.

What Types of Insurance Are Available Without a Business License?

Certain types of insurance are more accessible without a business license, particularly for individuals or small-scale operations. These include:

- Personal Liability Insurance: Covers individuals for risks related to their business activities, even without a formal license.

- Freelancer Insurance: Designed for independent workers who may not have a business license but need coverage for their work.

- Event Insurance: Temporary coverage for specific events or projects, often available without a business license.

Why Do Some Insurers Require a Business License?

Insurers may require a business license to verify the legitimacy and legal status of your business. This helps them assess risks and ensure compliance with local regulations. Reasons include:

- Risk Assessment: A business license indicates that your operations meet legal standards, reducing the insurer's risk.

- Legal Compliance: Ensures your business adheres to local laws, which can impact insurance claims.

- Business Credibility: A license demonstrates that your business is recognized and authorized to operate.

What Are the Alternatives If You Don’t Have a Business License?

If you lack a business license, there are still ways to secure insurance coverage. Consider the following options:

- Personal Insurance Policies: Some personal insurance policies may extend coverage to small business activities.

- Freelancer-Specific Plans: Many insurers offer tailored plans for freelancers or independent contractors.

- Temporary or Project-Based Coverage: Short-term insurance options for specific projects or events.

What Should You Consider Before Getting Insurance Without a Business License?

Before pursuing insurance without a business license, evaluate the following factors to ensure you make an informed decision:

- Legal Requirements: Check if your local laws allow operating without a business license.

- Coverage Limitations: Understand the scope of coverage and any exclusions that may apply.

- Insurer Policies: Research insurers that are flexible with licensing requirements.

Can you get insurance for a business without an LLC?

What Types of Business Insurance Are Available Without an LLC?

Yes, you can obtain business insurance even if your business is not structured as an LLC. Many insurance providers offer policies tailored to different business structures, including sole proprietorships, partnerships, and corporations. Here are some common types of insurance available:

- General Liability Insurance: Protects against claims of bodily injury, property damage, and advertising injury.

- Professional Liability Insurance: Covers claims related to professional errors or negligence.

- Commercial Property Insurance: Safeguards your business property, including equipment and inventory.

- Workers' Compensation Insurance: Required in most states if you have employees, covering work-related injuries or illnesses.

- Business Owner's Policy (BOP): Combines general liability and property insurance into one package, often at a lower cost.

Why Would a Business Without an LLC Need Insurance?

Even without an LLC, businesses face risks that can lead to significant financial losses. Insurance provides a safety net to protect your personal and business assets. Here are key reasons why insurance is essential:

- Legal Protection: Shields you from lawsuits or claims that could arise from accidents or errors.

- Financial Security: Covers unexpected expenses, such as property damage or medical bills for injured employees.

- Client Requirements: Many clients or contracts may require proof of insurance before doing business.

- Peace of Mind: Ensures you can focus on running your business without constant worry about potential risks.

How Does Business Insurance Differ for Non-LLC Entities?

Insurance for non-LLC businesses, such as sole proprietorships or partnerships, may differ in terms of coverage and liability. Here’s how:

- Personal Liability: Without an LLC, your personal assets may be at risk in lawsuits, making liability coverage crucial.

- Policy Customization: Insurance providers may tailor policies to suit the specific needs of your business structure.

- Cost Variations: Premiums may vary based on the level of risk associated with your business type.

What Are the Risks of Operating Without Business Insurance?

Operating a business without insurance exposes you to significant risks, especially if you don’t have the liability protection of an LLC. Consider the following:

- Lawsuits: Without insurance, you may have to pay legal fees and settlements out of pocket.

- Property Loss: Damage to your business property could result in costly repairs or replacements.

- Business Interruption: Unexpected events, like natural disasters, could halt operations and lead to lost income.

How to Choose the Right Insurance for a Non-LLC Business?

Selecting the right insurance for your non-LLC business involves assessing your specific needs and risks. Follow these steps:

- Evaluate Risks: Identify potential risks, such as property damage, liability claims, or employee injuries.

- Compare Policies: Research and compare insurance policies from multiple providers to find the best coverage.

- Consult an Expert: Work with an insurance agent or broker to ensure you understand your options and requirements.

- Review Regularly: Periodically reassess your insurance needs as your business grows or changes.

Do you need business insurance for a small business?

What is Business Insurance and Why is it Important?

Business insurance is a type of coverage designed to protect businesses from financial losses due to unforeseen events. For small businesses, it is particularly important because they often lack the financial resources to recover from significant losses. Business insurance can cover a variety of risks, including property damage, liability claims, and employee-related risks. Without adequate insurance, a small business could face severe financial hardship or even bankruptcy in the event of a major incident.

- Property Damage: Covers damage to business property due to fire, theft, or natural disasters.

- Liability Claims: Protects against claims of bodily injury or property damage caused by your business operations.

- Employee-Related Risks: Includes workers' compensation and employee benefits, ensuring your workforce is protected.

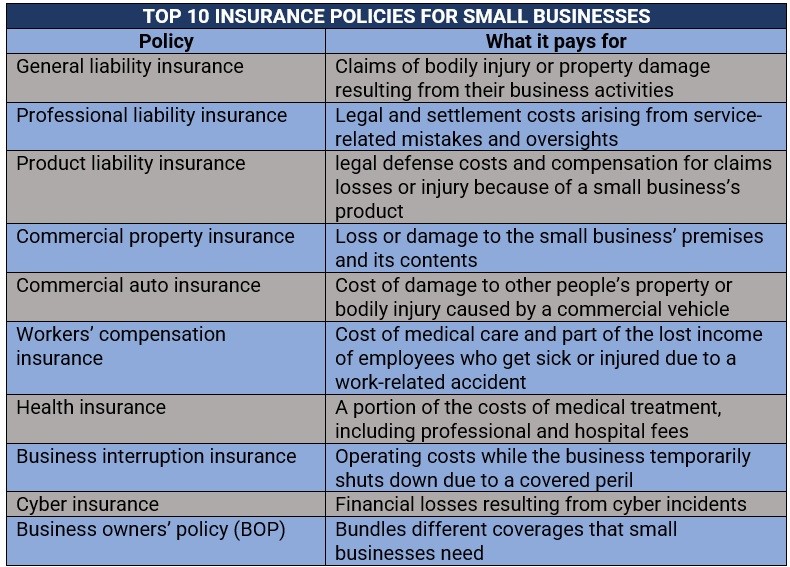

Types of Business Insurance for Small Businesses

There are several types of business insurance policies tailored to meet the specific needs of small businesses. The most common types include general liability insurance, professional liability insurance, and commercial property insurance. Each type of insurance serves a different purpose and provides coverage for various risks that a small business might face.

- General Liability Insurance: Covers third-party claims of bodily injury, property damage, and advertising injury.

- Professional Liability Insurance: Protects against claims of negligence or errors in professional services provided.

- Commercial Property Insurance: Provides coverage for physical assets like buildings, equipment, and inventory.

Legal Requirements for Business Insurance

In many jurisdictions, certain types of business insurance are legally required. For example, workers' compensation insurance is mandatory in most states if you have employees. Additionally, some industries may require specific types of insurance, such as professional liability insurance for healthcare providers. Failing to comply with these legal requirements can result in fines, penalties, or even the closure of your business.

- Workers' Compensation: Mandatory in most states if you have employees, covering work-related injuries or illnesses.

- Professional Liability Insurance: Often required for professions like doctors, lawyers, and consultants.

- Commercial Auto Insurance: Necessary if your business uses vehicles for operations.

Cost of Business Insurance for Small Businesses

The cost of business insurance varies depending on several factors, including the type of coverage, the size of the business, and the industry. Small businesses typically pay less for insurance compared to larger corporations, but the cost can still be significant. It's important to shop around and compare quotes from different insurers to find the best coverage at the most affordable price.

- Type of Coverage: More comprehensive policies will generally cost more.

- Business Size: Larger businesses with more employees or higher revenue may face higher premiums.

- Industry: High-risk industries like construction or healthcare may have higher insurance costs.

How to Choose the Right Business Insurance

Choosing the right business insurance involves assessing your business's specific risks and needs. Start by identifying the types of risks your business is most likely to face, such as property damage, liability claims, or employee-related issues. Then, consult with an insurance agent or broker who can help you tailor a policy that provides adequate coverage without unnecessary expenses.

- Assess Risks: Identify the most significant risks your business faces.

- Consult an Expert: Work with an insurance agent or broker to find the best policy.

- Compare Quotes: Get multiple quotes to ensure you're getting the best value for your coverage.

Can you get in trouble for not having business insurance?

What Are the Legal Consequences of Not Having Business Insurance?

Operating a business without the necessary insurance can lead to significant legal consequences. Depending on your location and industry, certain types of insurance, such as workers' compensation or general liability insurance, may be legally required. If you fail to comply, you could face:

- Fines and penalties imposed by regulatory authorities.

- Lawsuits from employees, customers, or third parties for damages or injuries.

- Business closure if you are unable to meet legal requirements.

How Does Lack of Business Insurance Affect Financial Stability?

Not having business insurance can severely impact your financial stability. Without coverage, you may be personally liable for:

- Legal fees and settlements in case of lawsuits.

- Medical expenses if an employee or customer is injured on your premises.

- Property damage costs if your business assets are damaged or destroyed.

Can You Lose Contracts or Clients Without Business Insurance?

Many clients and partners require proof of business insurance before entering into contracts. Without it, you risk:

- Losing contracts with clients who mandate insurance coverage.

- Damaging your reputation as a reliable business partner.

- Missing out on opportunities in industries where insurance is a standard requirement.

What Happens If an Employee Gets Injured Without Workers' Compensation Insurance?

If an employee is injured and you lack workers' compensation insurance, you may face:

- Legal action from the injured employee for medical expenses and lost wages.

- Hefty fines from government agencies for non-compliance.

- Personal financial liability if you are unable to cover the costs out of pocket.

Are There Industry-Specific Risks for Not Having Business Insurance?

Certain industries have higher risks associated with not having business insurance. For example:

- Construction companies may face lawsuits for workplace accidents or property damage.

- Healthcare providers risk malpractice claims without professional liability insurance.

- Retail businesses may suffer losses from theft, fire, or customer injuries.

Frequently Asked Questions

Can you get business insurance without a business license?

Yes, in some cases, you can obtain business insurance without having a business license. However, this depends on the type of business you operate, the insurance provider, and the specific requirements of your state or country. Some insurers may offer coverage to freelancers, independent contractors, or small businesses that are in the process of obtaining a license. It's important to note that operating without a license may limit your insurance options and could affect the validity of your policy if discovered later.

What types of business insurance can you get without a business license?

Certain types of business insurance, such as general liability insurance or professional liability insurance, may be available without a business license. These policies are often designed to protect against third-party claims, such as bodily injury, property damage, or professional errors. However, other types of insurance, like workers' compensation or commercial auto insurance, may require proof of a valid business license before coverage is granted. Always check with the insurer to understand their specific requirements.

Why do some insurance companies require a business license?

Insurance companies often require a business license to verify that your business is legally recognized and operating within the law. A license serves as proof that your business complies with local regulations, which reduces the insurer's risk. Additionally, a license may be necessary to determine the appropriate coverage and premiums for your business. Without a license, insurers may view your business as higher risk, which could lead to higher costs or denial of coverage.

What are the risks of getting business insurance without a license?

Obtaining business insurance without a business license can pose several risks. First, your policy may be deemed invalid if the insurer discovers you are operating without a license, leaving you unprotected in the event of a claim. Second, you may face legal penalties for operating an unlicensed business, depending on your jurisdiction. Lastly, some clients or partners may require proof of a valid license before working with you, which could limit your business opportunities. It's always advisable to obtain the necessary licenses before seeking insurance coverage.

Leave a Reply

Our Recommended Articles