Starting an insurance company as a sole proprietor is an ambitious endeavor that requires careful planning and a thorough understanding of legal, financial, and regulatory requirements. While the insurance industry is highly regulated, it is not impossible to establish a business as a sole proprietor. This article explores the feasibility of launching an insurance company under this business structure, examining the challenges, advantages, and steps involved. From obtaining the necessary licenses to managing risks and building a client base, we’ll provide insights to help you determine if this path aligns with your entrepreneurial goals and resources.

- Can I Start an Insurance Company as a Sole Proprietor?

- 1. What Are the Legal Requirements for Starting an Insurance Company?

- 2. What Are the Financial Requirements for an Insurance Company?

- 3. What Types of Insurance Can a Sole Proprietor Offer?

- 4. What Are the Risks of Starting an Insurance Company as a Sole Proprietor?

- 5. How Can a Sole Proprietor Market an Insurance Company?

- Can I get business insurance as a sole proprietor?

- Can an individual own an insurance company?

- Can an individual legally own an insurance company?

- What are the financial requirements for owning an insurance company?

- What types of insurance can an individual-owned company offer?

- What are the challenges of owning an insurance company as an individual?

- How does an individual start an insurance company?

- Which legal entity is best for your insurance agency?

- Can I get business insurance without an LLC?

- Frequently Asked Questions from Our Community

Can I Start an Insurance Company as a Sole Proprietor?

Starting an insurance company as a sole proprietor is possible, but it comes with significant challenges and regulatory requirements. A sole proprietorship is the simplest business structure, where the owner is personally responsible for all aspects of the business. However, the insurance industry is highly regulated, and starting an insurance company requires compliance with state and federal laws, obtaining necessary licenses, and meeting financial requirements. Below, we explore key aspects of starting an insurance company as a sole proprietor.

1. What Are the Legal Requirements for Starting an Insurance Company?

To start an insurance company as a sole proprietor, you must comply with legal requirements set by your state's insurance department. This includes obtaining an insurance license, which often requires passing an exam and completing pre-licensing education. Additionally, you must register your business with the state and adhere to specific regulations regarding capital requirements and reserves. Failure to meet these requirements can result in penalties or the inability to operate.

See Also How to Get Sponsors for a Team

How to Get Sponsors for a Team2. What Are the Financial Requirements for an Insurance Company?

Starting an insurance company requires significant financial resources. As a sole proprietor, you must demonstrate that you have sufficient capital to cover potential claims and operational expenses. Most states require a minimum amount of capital and surplus to ensure the company can meet its obligations. Additionally, you may need to purchase reinsurance to protect against large claims. Below is a table summarizing common financial requirements:

| Requirement | Description |

|---|---|

| Minimum Capital | Varies by state; typically ranges from $100,000 to $1 million. |

| Surplus Funds | Additional funds to cover unexpected claims or losses. |

| Reinsurance | Insurance for your insurance company to mitigate large risks. |

3. What Types of Insurance Can a Sole Proprietor Offer?

As a sole proprietor, you can offer various types of insurance, such as auto insurance, homeowners insurance, health insurance, or life insurance. However, the type of insurance you offer will determine the specific licenses and certifications you need. For example, selling health insurance may require additional certifications compared to selling auto insurance. It's essential to research the requirements for each type of insurance you plan to offer.

4. What Are the Risks of Starting an Insurance Company as a Sole Proprietor?

Starting an insurance company as a sole proprietor carries significant risks. Since a sole proprietorship does not provide liability protection, you are personally responsible for any debts or legal claims against the business. This means your personal assets, such as your home or savings, could be at risk if the company faces financial difficulties or lawsuits. Additionally, the insurance industry is highly competitive, and establishing a client base can be challenging.

See Also Which Angels or Vcs Will Fund Hardware Startups?

Which Angels or Vcs Will Fund Hardware Startups?5. How Can a Sole Proprietor Market an Insurance Company?

Marketing is crucial for the success of an insurance company. As a sole proprietor, you can use strategies such as digital marketing, social media advertising, and networking to attract clients. Building a strong online presence through a professional website and engaging content can help establish credibility. Additionally, partnering with local businesses or offering referral incentives can help grow your client base. Below is a table summarizing effective marketing strategies:

| Strategy | Description |

|---|---|

| Digital Marketing | Use SEO, PPC, and email campaigns to reach potential clients. |

| Social Media | Engage with clients on platforms like Facebook, LinkedIn, and Instagram. |

| Networking | Attend industry events and build relationships with other professionals. |

| Referral Incentives | Offer discounts or rewards for client referrals. |

Can I get business insurance as a sole proprietor?

What Types of Business Insurance Are Available for Sole Proprietors?

As a sole proprietor, you have access to various types of business insurance to protect your business and personal assets. Some common options include:

See Also How Can One Start a Venture With No Money?

How Can One Start a Venture With No Money?- General Liability Insurance: Covers third-party claims for bodily injury, property damage, and advertising injury.

- Professional Liability Insurance: Protects against claims of negligence or errors in your professional services.

- Commercial Property Insurance: Safeguards your business property, such as equipment, inventory, or office space.

- Business Interruption Insurance: Provides financial support if your business operations are disrupted due to covered events.

- Workers' Compensation Insurance: Required if you have employees, covering medical expenses and lost wages for work-related injuries.

Why Do Sole Proprietors Need Business Insurance?

Even as a sole proprietor, having business insurance is crucial for several reasons:

- Legal Protection: Shields you from lawsuits or claims that could arise from your business activities.

- Financial Security: Prevents out-of-pocket expenses for damages, legal fees, or settlements.

- Client Requirements: Many clients or contracts may require proof of insurance before working with you.

- Asset Protection: Separates your personal and business liabilities, safeguarding your personal assets.

- Peace of Mind: Allows you to focus on growing your business without worrying about potential risks.

How Much Does Business Insurance Cost for Sole Proprietors?

The cost of business insurance for sole proprietors varies depending on several factors:

- Type of Coverage: General liability insurance is typically more affordable than professional liability or property insurance.

- Industry Risks: High-risk industries, such as construction, may have higher premiums.

- Business Size: Larger operations or higher revenue may increase insurance costs.

- Location: Insurance rates can vary based on your geographic area and local regulations.

- Claims History: A history of claims may result in higher premiums.

Can Sole Proprietors Bundle Insurance Policies?

Yes, sole proprietors can often bundle multiple insurance policies into a Business Owner's Policy (BOP), which offers several advantages:

- Cost Savings: Bundling policies usually results in lower premiums compared to purchasing them separately.

- Simplified Management: Managing one policy is easier than handling multiple policies from different providers.

- Comprehensive Coverage: A BOP typically includes general liability, property insurance, and business interruption coverage.

- Customizable Options: You can add additional coverages, such as professional liability or cyber insurance, to suit your needs.

- Convenience: Streamlines the process of obtaining and renewing insurance.

What Should Sole Proprietors Consider When Choosing Business Insurance?

When selecting business insurance, sole proprietors should evaluate the following factors:

- Business Risks: Identify the specific risks associated with your industry and operations.

- Coverage Limits: Ensure the policy provides adequate coverage for potential claims or losses.

- Deductibles: Choose a deductible amount that balances affordability and financial protection.

- Provider Reputation: Research the insurer's reputation, customer service, and claims process.

- Policy Exclusions: Review what is not covered to avoid surprises during a claim.

Can an individual own an insurance company?

Can an individual legally own an insurance company?

Yes, an individual can legally own an insurance company, but it requires compliance with strict regulations and licensing. The process involves:

- Obtaining the necessary licenses from regulatory authorities, which vary by country or state.

- Meeting capital requirements to ensure financial stability and the ability to pay claims.

- Adhering to legal and operational guidelines set by insurance regulators.

What are the financial requirements for owning an insurance company?

Starting an insurance company requires significant financial resources. Key considerations include:

- Minimum capital requirements, which can range from hundreds of thousands to millions of dollars depending on the jurisdiction.

- Reserve funds to cover potential claims and ensure solvency.

- Operational costs, such as staffing, technology, and marketing expenses.

What types of insurance can an individual-owned company offer?

An individual-owned insurance company can offer various types of insurance, including:

- Life insurance, which provides financial protection to beneficiaries upon the policyholder's death.

- Health insurance, covering medical expenses and treatments.

- Property and casualty insurance, protecting against damage to property or liability for injuries.

What are the challenges of owning an insurance company as an individual?

Owning an insurance company as an individual comes with several challenges:

- Regulatory compliance, which requires ongoing adherence to complex laws and regulations.

- Risk management, as the company must be prepared to handle large claims and financial uncertainties.

- Market competition, as established companies dominate the industry.

How does an individual start an insurance company?

Starting an insurance company involves several steps:

- Conduct market research to identify a niche or demand in the market.

- Develop a business plan outlining the company's structure, goals, and financial projections.

- Secure funding to meet capital requirements and operational expenses.

- Obtain licenses and approvals from regulatory bodies.

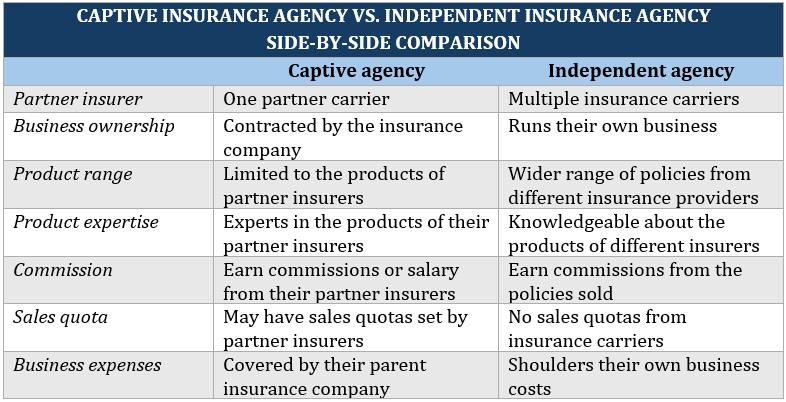

Which legal entity is best for your insurance agency?

Understanding the Different Legal Entities for Insurance Agencies

Choosing the right legal entity for your insurance agency is crucial for liability protection, tax benefits, and operational flexibility. The most common options include:

- Sole Proprietorship: Simple to set up but offers no personal liability protection.

- Partnership: Ideal for shared ownership but requires clear agreements to avoid disputes.

- Limited Liability Company (LLC): Combines liability protection with tax flexibility.

- Corporation (S-Corp or C-Corp): Provides strong liability protection but involves more regulatory requirements.

Factors to Consider When Choosing a Legal Entity

When deciding on the best legal structure for your insurance agency, consider the following factors:

- Liability Protection: Ensure your personal assets are shielded from business liabilities.

- Tax Implications: Evaluate how each entity affects your tax obligations and potential savings.

- Operational Complexity: Assess the administrative burden and compliance requirements.

- Growth Potential: Choose a structure that supports future expansion and investment opportunities.

Pros and Cons of an LLC for Insurance Agencies

An LLC is a popular choice for insurance agencies due to its balance of liability protection and tax benefits. Here are its advantages and disadvantages:

- Pros: Limited liability, pass-through taxation, and operational flexibility.

- Cons: Higher formation costs and potential self-employment taxes.

Why Corporations Might Be Suitable for Larger Insurance Agencies

For larger insurance agencies, a corporation (S-Corp or C-Corp) may be more appropriate due to its ability to handle significant growth and attract investors. Key points include:

- Liability Protection: Shareholders are not personally liable for business debts.

- Tax Benefits: Potential for lower self-employment taxes with an S-Corp.

- Investor Appeal: Easier to raise capital through stock issuance.

How to Transition Your Insurance Agency to a Different Legal Entity

If your current legal structure no longer suits your insurance agency, transitioning to a new entity involves several steps:

- Consult a Legal Professional: Ensure compliance with state and federal regulations.

- File Necessary Documents: Submit articles of incorporation or organization to the appropriate authorities.

- Update Contracts and Licenses: Notify clients, vendors, and regulatory bodies of the change.

- Adjust Tax Filings: Update your tax status with the IRS and state agencies.

Can I get business insurance without an LLC?

What Types of Business Insurance Are Available Without an LLC?

Yes, you can obtain business insurance without forming an LLC. Many types of insurance policies are available to sole proprietors, freelancers, and other business structures. Here are some common options:

- General Liability Insurance: Protects against third-party claims for bodily injury, property damage, and advertising injuries.

- Professional Liability Insurance: Covers claims related to errors, negligence, or malpractice in professional services.

- Commercial Property Insurance: Safeguards your business property, including equipment, inventory, and office space.

- Business Owner’s Policy (BOP): Combines general liability and property insurance into one package, often at a lower cost.

- Workers’ Compensation Insurance: Required if you have employees, regardless of your business structure.

Why Do You Need Business Insurance Without an LLC?

Even without an LLC, business insurance is essential to protect your personal and professional assets. Here’s why:

- Personal Asset Protection: Without an LLC, your personal assets are at risk if your business faces a lawsuit.

- Client Requirements: Many clients or contracts may require proof of insurance before working with you.

- Risk Management: Insurance helps mitigate risks associated with accidents, lawsuits, or property damage.

- Credibility: Having insurance can enhance your business’s credibility and professionalism.

- Financial Security: It provides a safety net for unexpected events that could otherwise devastate your business.

How Does Business Insurance Work for Sole Proprietors?

For sole proprietors, business insurance functions similarly to other business structures. Here’s how it works:

- Policy Customization: You can tailor policies to fit your specific business needs and risks.

- Premiums: Costs depend on factors like your industry, coverage limits, and business size.

- Claims Process: If a claim arises, you file it with your insurer, who assesses and pays for covered losses.

- Tax Deductions: Premiums are often tax-deductible as a business expense.

- No Legal Separation: Since sole proprietors and their businesses are not legally separate, insurance is crucial for personal protection.

What Are the Risks of Operating Without Business Insurance?

Operating without business insurance exposes you to significant risks, especially without an LLC. Consider the following:

- Lawsuits: You could face costly legal battles if a client or third party sues your business.

- Property Damage: Without insurance, you’d bear the full cost of repairing or replacing damaged property.

- Medical Expenses: If someone is injured on your premises, you may be liable for their medical bills.

- Business Interruption: Unexpected events like fires or natural disasters could halt operations without coverage.

- Personal Financial Loss: Your personal savings and assets could be at risk if your business faces a major claim.

How to Choose the Right Business Insurance Without an LLC?

Selecting the right business insurance requires careful consideration. Follow these steps:

- Assess Your Risks: Identify the specific risks associated with your business operations.

- Compare Policies: Research and compare different insurance providers and their offerings.

- Consult an Agent: Work with an insurance agent to understand your options and get tailored advice.

- Review Coverage Limits: Ensure the policy covers potential losses adequately.

- Check for Exclusions: Understand what is not covered to avoid surprises during a claim.

Frequently Asked Questions from Our Community

Can I legally start an insurance company as a sole proprietor?

Yes, you can legally start an insurance company as a sole proprietor, but it depends on the regulations in your jurisdiction. In many countries, the insurance industry is highly regulated, and you may need to obtain specific licenses and meet certain capital requirements. Additionally, you may need to comply with strict legal and financial standards to ensure you can cover potential claims. It's crucial to consult with a legal expert or regulatory body in your area to understand the exact requirements.

What are the advantages of starting an insurance company as a sole proprietor?

Starting an insurance company as a sole proprietor offers several advantages. First, you have full control over all business decisions, allowing you to shape the company according to your vision. Second, the startup costs and administrative requirements are often lower compared to forming a corporation or partnership. Additionally, as a sole proprietor, you can enjoy simpler tax filing processes, as your business income is typically reported on your personal tax return. However, these benefits come with the trade-off of unlimited personal liability for any debts or claims against the business.

What are the risks of operating an insurance company as a sole proprietor?

Operating an insurance company as a sole proprietor carries significant risks. The most notable is unlimited personal liability, meaning your personal assets could be at risk if the company faces lawsuits or financial difficulties. Additionally, the insurance industry is highly competitive and requires substantial financial reserves to cover potential claims. As a sole proprietor, you may also face challenges in raising capital or securing partnerships due to the perceived risk of your business structure. It's essential to have a solid risk management plan and consider purchasing liability insurance to protect yourself.

What steps are required to start an insurance company as a sole proprietor?

To start an insurance company as a sole proprietor, you must first conduct thorough market research to identify your target audience and niche. Next, you'll need to obtain the necessary licenses and permits from regulatory authorities, which may include passing exams or meeting specific educational requirements. You'll also need to establish a business plan outlining your services, pricing, and financial projections. Additionally, securing adequate capital to cover operational costs and potential claims is critical. Finally, you should set up a business bank account, purchase necessary insurance policies, and ensure compliance with all local and federal regulations.

Leave a Reply

Our Recommended Articles